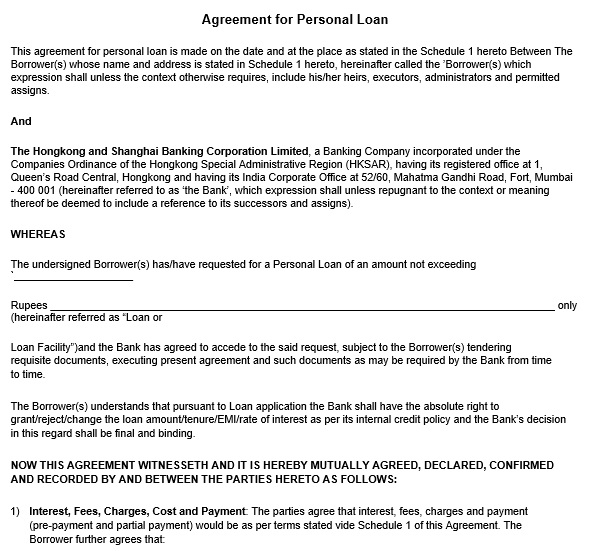

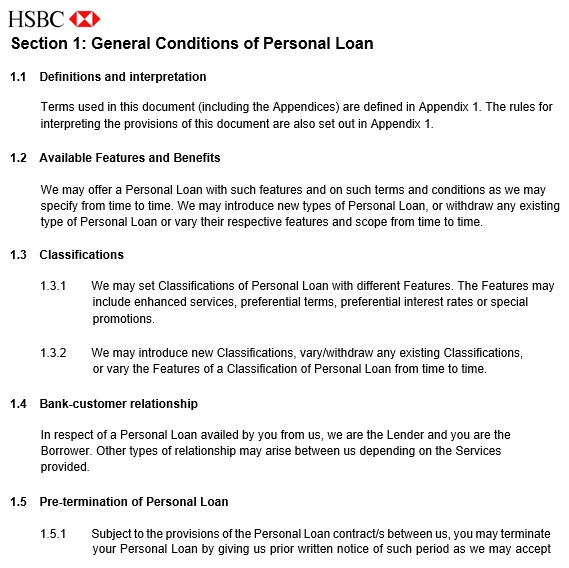

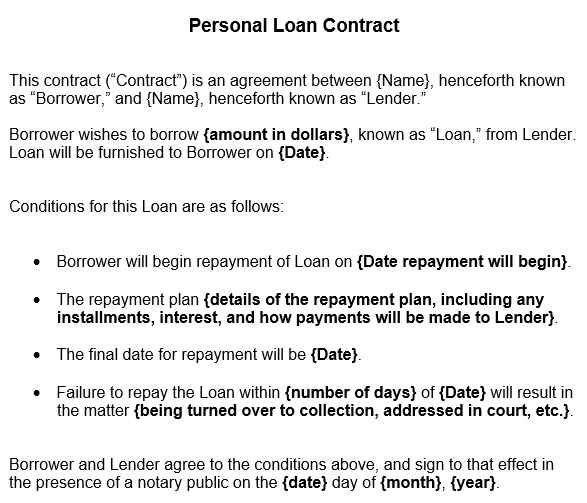

A personal loan template is a legal document that contains the terms and conditions of a personal loan. A personal loan includes a certain amount of money borrowed by a person. It is the responsibility of the borrower to pay you back along with the interest rate as per the terms of the contract. You must create a personal loan agreement in order to give a personal loan to someone.

The types of personal loans you will agree too:

Co-sign:

When the borrower has no credit or poor credit and another person takes the responsibility in case the borrower can’t pay.

Fixed rate:

Here, during the entire course of the loan’s repayment period, the interest rate won’t change.

Secured:

In case of default, the borrower should put up collateral. A second mortgage on their home or their car is the most common collateral example.

Unsecured:

For borrower, there is no need to put up collateral as part of the agreement. This is because, in case of default, their personal assets may still get confiscated legally.

Variable rate:

Variable rate includes the third-party that sets the interest rates.

What are the 3 parts of a loan?

Before making any decisions, for the borrower, it is essential to understand the fundamental principles of loaning. The lender should familiarize with these principles. There are 3 main parts of a loan;

Interest rate:

The amount that you charge for borrowing money is known as interest rate and it is usually considered a small percentage of the loan amount. Interest rate is further classified into two;

- Fixed rates that can’t change

- Variable rates can change during the overall course of the repayment period.

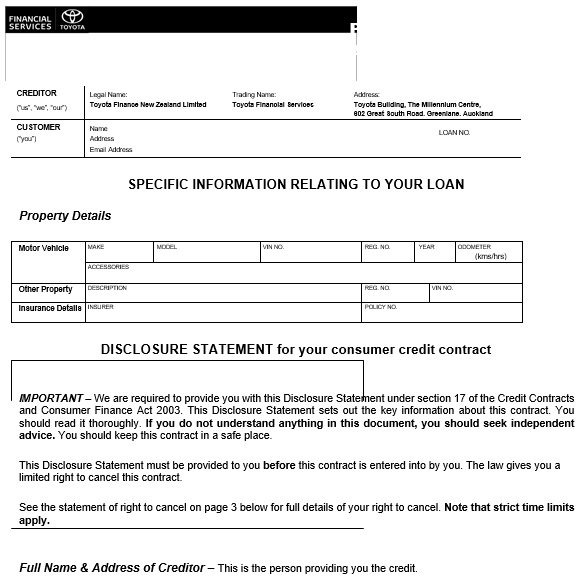

Security component:

The security component refers to the assets or collateral that the borrower puts up to guarantee the loan. Here are the two types of loans;

- In a secured loan, the borrower guarantees the lender that he will get repaid. In case, the borrower fails to pay the loan then to get back your investment, you can take possession of the collateral. This type of loan allows you to charge a lower interest rate.

- An unsecured loan doesn’t require any collateral to put up from the borrower. If the borrower defaults on the loan then you don’t have protection. As compared to a secured loan, the unsecured loan has high-interest rate.

Term:

Term refers to the amount of time that the borrower has to pay back the loan. However, the common term is between 1 and 5 years and longer terms refer higher interest rates.

Questions to ask to the borrower before making a personal loan template:

You should ask the following questions to the borrower;

What do you require the money for?

The lender has the right to know for what purpose the borrower requires the money. It is suggested to refer the borrower to the nearest lending institution if you believe the reason isn’t enough.

How long the borrower will take to pay the loan back?

You can feel comfortable charging zero-interest if the loan is just a necessity until the borrower’s next paycheck. There is no need for a personal loan form. But, in case, if the loan involves a significant amount and borrower requires months to pay it off then you must create a written document.

What is the borrower current financial status?

Before agreeing to the loan, as a lender, it is your responsibility to find out whether the borrower is in an adequate financial situation. The situation may be considered an awkward one but keep in mind that the borrower approached you for the money.

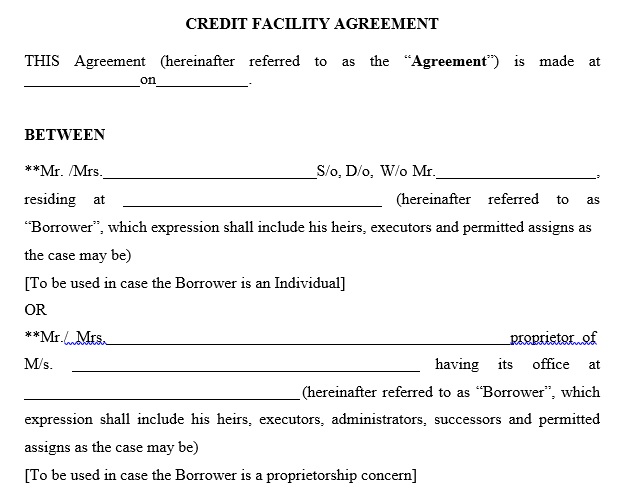

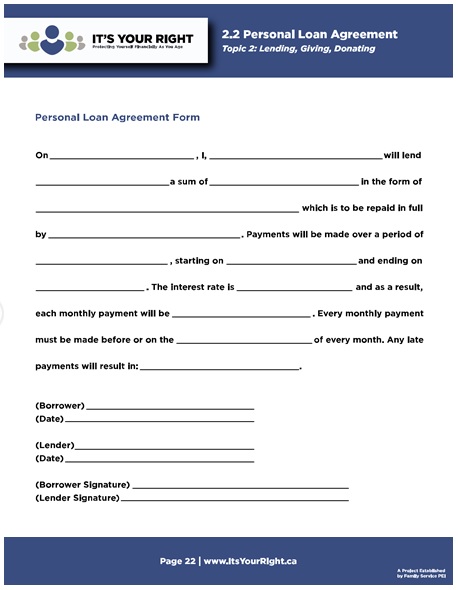

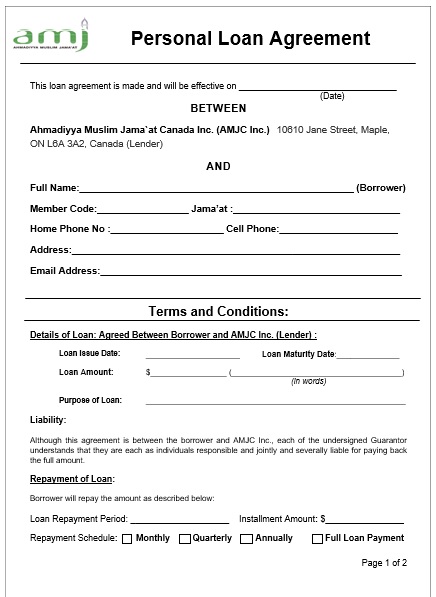

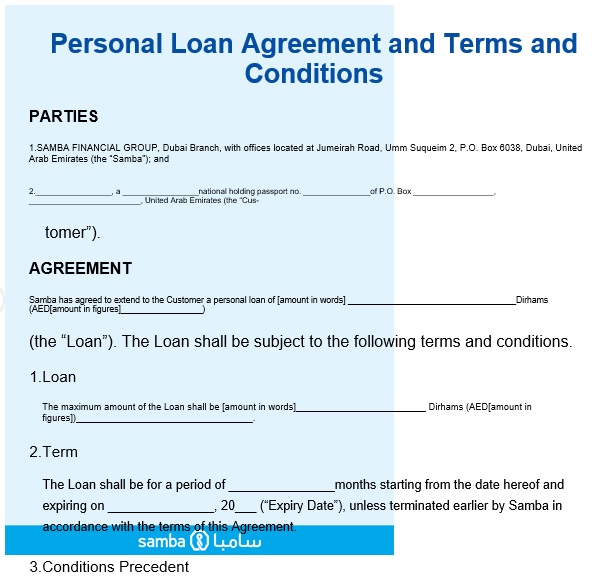

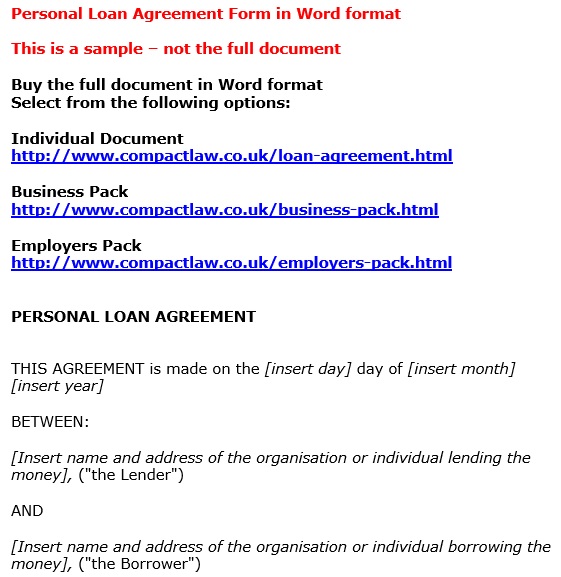

How to write a personal loan agreement?

You have to include the following elements in your personal loan agreement;

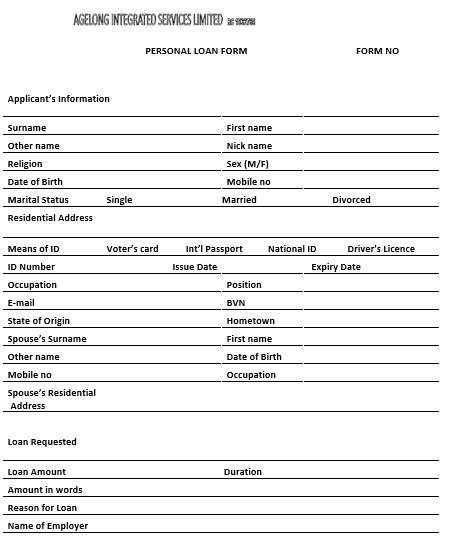

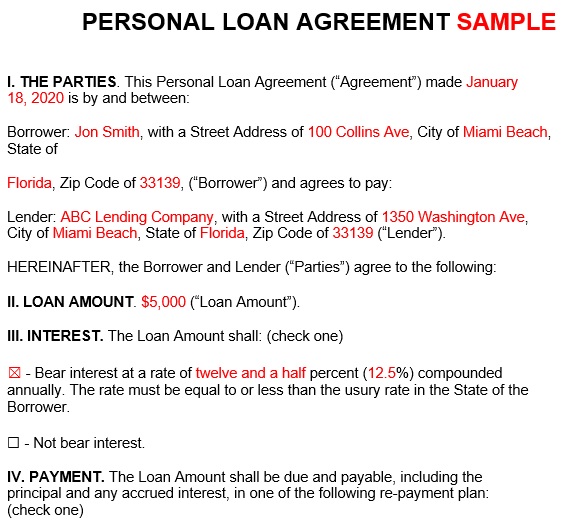

Personal details:

This section should include the following;

- The complete names

- Addresses

- Contact details of yourself

- The borrower

Date:

Include the date that when the agreement is created.

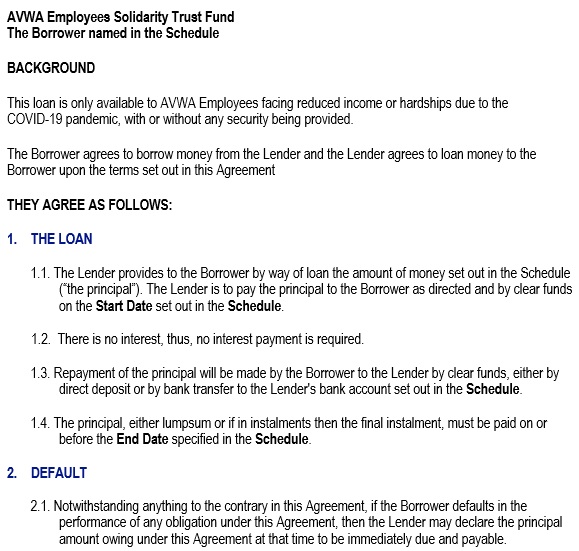

Loan amount:

Here, you have to include the total amount that the borrower loan from you.

Repayment details:

State in the agreement whether the borrower is agreed to pay you back periodically or with a lump sum.

Interest rate:

Mention the agreed-upon interest rate in your agreement.

Late payments and outcomes of defaulting:

The agreement should specify when you will consider the loan payments late. Also, indicates the implications of these late payments. For instance, the late payments result in late fees. It is recommended also specify the amounts. If the borrower violates any terms of your agreement, specify what happens then.

Guarantor details:

If the borrower has any guarantor then he should also sign the document. The guarantor refers to the third party who will repay the loan in case the borrower fails to pay back. Guarantor is not a requirement for a personal loan but it will provide you a greater sense of security.

Who requires a loan agreement?

Usually, loans occur between family members. But, a loan agreement can also be used among organizations or entities conducting a business relationship.

- Here is a list of possible lenders who might require this agreement;

- Seller of a home

- Seller of a car

- Investor

- Family member

- Sympathetic friend having extra funds

Here is a list of the possible borrower who might require this agreement;

- Buyer of a home

- Buyer of a car

- Startup Company

- Family member

- Reliable friend that has the unexpected fund

When should you use a loan agreement?

Whenever you lend or borrow money, you should use a loan agreement. Don’t rely only on a verbal promise if your payback terms are complicated. In a written agreement, both parties outlines clearly installment payment terms and the exact amount of interest owed.

The agreement has consequences that both parties have to face in case either of them not fulfill their side of the terms. You may need this agreement in the following situations;

- When you are going to start a business with a capital loan

- Buying land or a home with a real estate loan

- When you are going to invest in a college education or repaying a student loan

- Purchasing a new car or boat

- If you want to assist a friend or family member out with a personal loan

Furthermore, a loan agreement assists you in identifying which lenders to avoid. Individual or entities who lend money at higher rates may be considered as loan sharks.

Conclusion:

In conclusion, a personal loan template is a legally binding contract between a borrower and a lender. This contract explains the terms of a personal loan. Generally, it involves the amount, payment details, the lender’s right, and should the borrower default on the loan.

Faqs (Frequently Asked Questions)

A personal loan agreement can be required by the;

1- Banks

2- Credit unions

3- Online lenders

4- Payday lenders

Yes, a personal loan agreement is legally binding. It doesn’t matter whether the lender is a financial institution or another individual. The consequences are the same in case lender or borrower default on the agreement.

A friendly loan agreement is more flexible than traditional ones. But, any changes made to agreement must be agreed by both parties and attached to the original agreement.